- Scale. Quantinuum priced at $60 per share — $5 above its original $53–$55 range — raising $1.68 billion in the largest quantum-computing IPO on record and valuing the company at roughly $16 billion.

- Sector moment. The listing lifted peers IonQ and D-Wave sharply, pulling quantum computing out of the pre-revenue category and into the same institutional portfolio discussions that AI names have dominated for two years.

- Policy backdrop. The Trump administration recently announced $2 billion in government equity stakes across nine quantum companies, including Quantinuum, making the sector a stated national-security priority alongside AI chips.

Honeywell’s quantum spinout Quantinuum made its Nasdaq debut on June 4, 2026, raising $1.68 billion after pricing 28 million shares at $60 each, above the company’s marketed range of $53 to $55. Shares opened at $68 and hit an intraday high of $71.35, before paring gains to close at $60.38 — essentially flat on the IPO price but leaving the company with a market capitalisation of approximately $16 billion based on shares outstanding in its filings. The ticker is QNT.

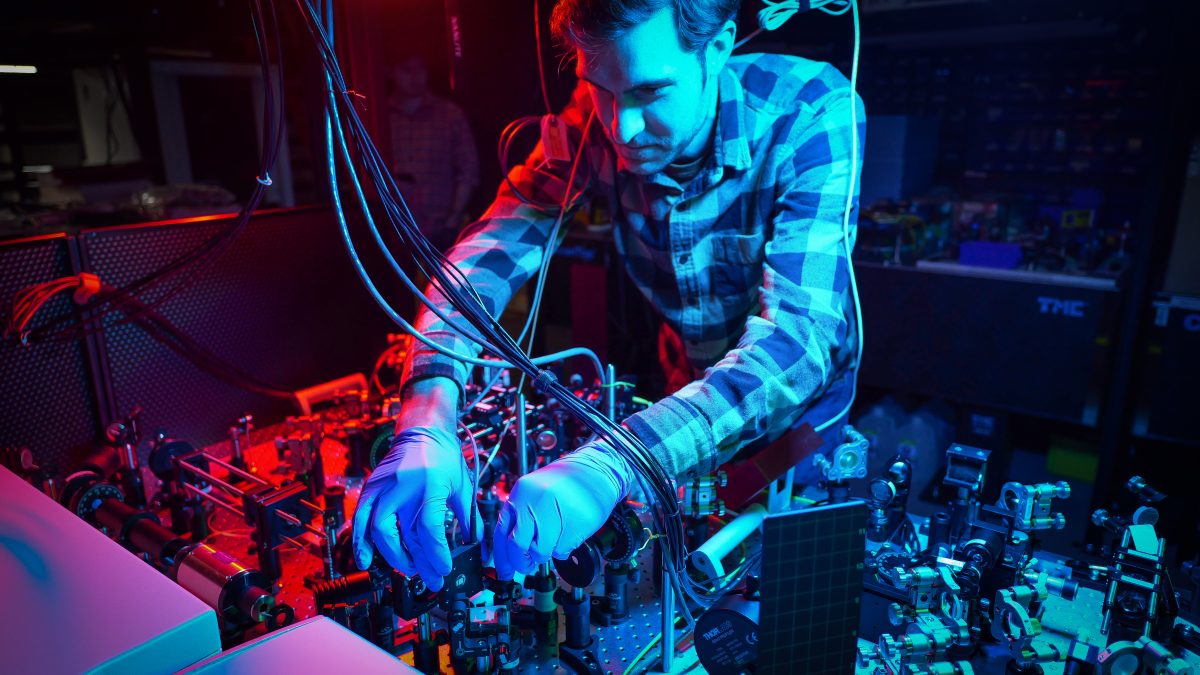

What Quantinuum actually is

Quantinuum was formed in 2021 from the merger of Honeywell’s internal quantum computing division with Cambridge Quantum, a UK-based quantum software company. The combination produced what management describes as a “full-stack” quantum platform — meaning the company builds both the physical hardware (trapped-ion quantum processors) and the algorithms and applications that run on top of them. That vertical integration distinguishes it from most listed quantum names, which are either pure hardware or pure software plays.

Honeywell retains approximately 48.1% of combined voting power post-IPO, giving it effective control while allowing outside investors to participate in the sector’s growth. Founder Ilyas Khan holds roughly 15% of the company, a stake worth more than $2 billion at the IPO valuation.

The capital market moment for quantum

Quantinuum’s listing arrives at a confluence of government support and investor appetite that would have been difficult to predict two years ago. The Trump administration’s $2 billion quantum equity programme — spread across nine companies — functioned as an implicit endorsement of the sector’s national-security relevance, echoing the policy rationale that drove semiconductor legislation earlier in the decade.

Analysts at Wedbush noted that “more quantum names reaching public markets deepens the universe, improves price discovery, and draws sellside and institutional coverage” — language that reflects a broader transition from the sector being a venture-capital curiosity to one that pension funds and index funds can evaluate. The flat close, while muted versus the intraday pop, is consistent with large institutional IPO allocations being flipped on opening day; the secondary-market price in coming weeks will be the more meaningful indicator of durable demand.

The SpaceX IPO, priced separately for its June 12 debut, at a $1.75 trillion valuation, has absorbed significant liquidity from the risk-on end of the market. That Quantinuum’s offering was upsized and oversubscribed despite that competition suggests the IPO window is broadly open and that quantum computing, despite still being pre-commercial at scale, has crossed a credibility threshold with the institutional investment community.